ROLE

Product Design

User Research

TIMELINE

11 weeks

[Summer 2025]

TOOLS

Figma

Figjam

OVERVIEW

Helping shape features across the product.

In the Summer of 2025, I joined SHB's Digital Transformation Team as a product design intern, contributing to three features on SHB SAHA — the bank's newly launched mobile banking app.

Over the summer, I worked on:

Cash flow & asset management features

Onboarding redesign for new credit offerings

Security Center research and discovery

CONTEXT

Designing for digital transformation.

As one of the leading commercial banks in Vietnam with over 30 years of history, Saigon-Hanoi Bank (SHB) is currently undergoing a massive digital transformation to better serve its growing customer base. Through their forward-thinking "Bank of the Future" initiative, SHB is actively modernizing its digital footprint to deliver a more accessible, seamless, and innovative mobile banking ecosystem.

I joined their core digital transformation team to work on the SAHA platform, where I was able to contribute to features that were considered core to the retail banking experience on their applications and support various other features.

PROBLEM SPACE

Vietnamese banking customers span a wide range of financial literacy levels, life stages, and relationships with money — from first-time savers to seasoned investors, from those who prioritize safety to those who spend freely. In order to design a comprehensive experience, we mapped users across two axes: where they are in their financial journey, and how they think about money.

This shaped two core design priorities — turning a user's own banking data into actionable insights, and building financial literacy progressively, from the basics to more advanced concepts, all within a single financial hub on the app.

SOLUTION

3 core features that focus on education, automation and insights

Through research spanning the bank's clientele, user interviews, and international journals, we focused on three features: Assets Overview, Cash Flow Tracking, and Financial Planning.

Together, they move users from simply staying informed, with minimal effort on their part , to receiving actionable insights and educational context that help them understand what the numbers mean and what to do next.

RESEARCH

Secondary research

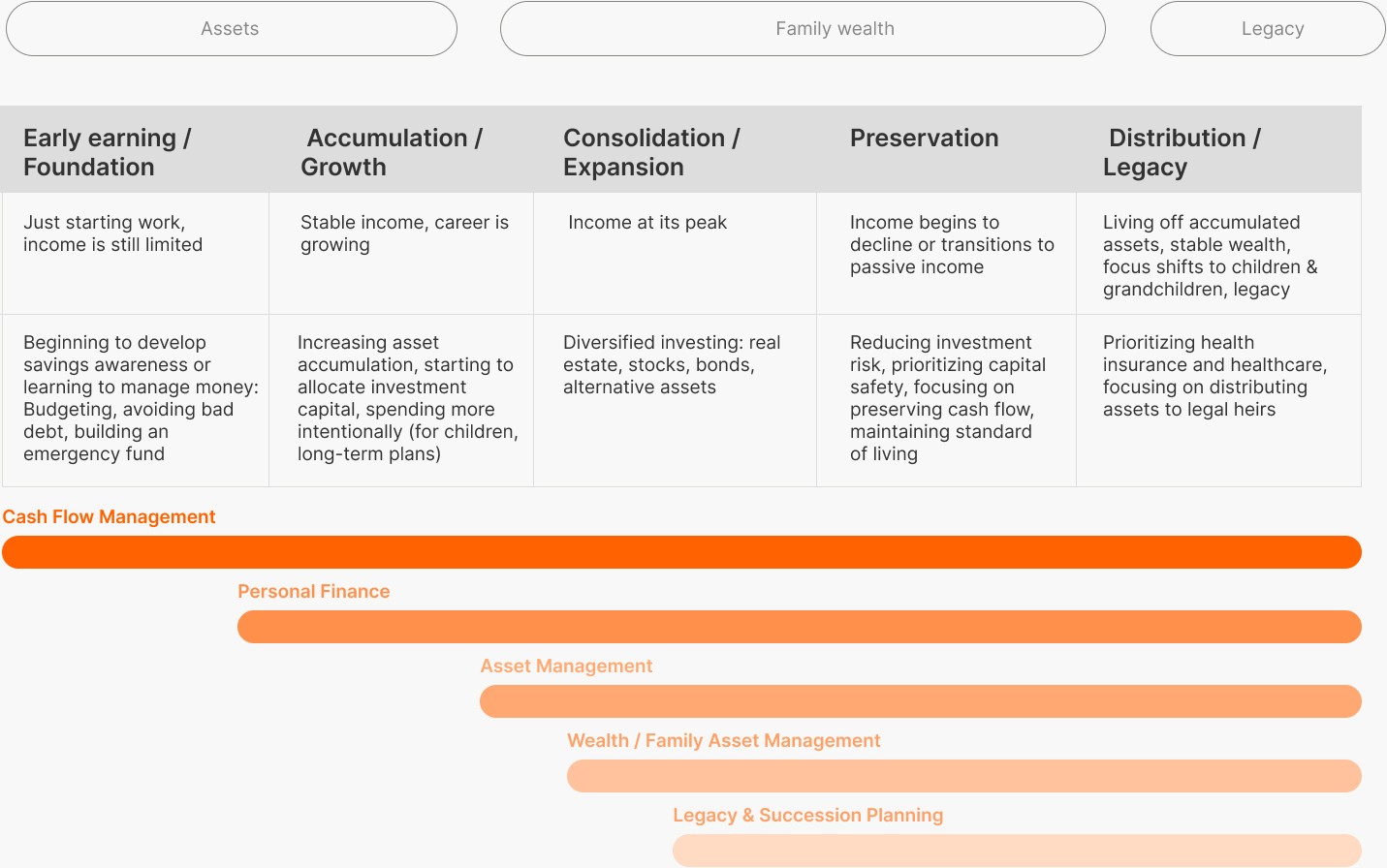

First, I started with researching national and international resources and reports on personal finance management. A concept that I was encouraged to dive deep in, based on an article by CFA on life cycles, is how each stage of a person's life correlates with certain financial needs and behaviours.

Lifecycle & Financial journey

However, as we looked into lifecycle and how this intersects with the typical user's financial journey and therefore their behavior, we realized that at the same stage of life, people have different mindsets when thinking about money.

We looked at data and articles, but in reality, upon reflecting on how the people around us deal with money, we realize that people can have the same amount of money and assets, in the same stages of their lives, and treat finance in completely different ways based on many different factors, including finacial literacy level, life goals, personalities, background and more, which can be summarized into mindsets.

Upon doing more secondary research, we decided on 3 most observable among our Vietnamese user base:

Competitive analysis

Primary research

From surveys + existing materials at SHB, we found:

Users mainly use SHB app for casual daily transactions

Daily transactions are the primary use case for most users, while loans and savings are secondary needs.

Accumulation is the primary mindset among most users

83% of SHB users focus on accumulation, prioritizing saving and growing money over spending or investing.

Users operate across multiple banking apps

Half of users have 3 banking apps active on their phone, with many managing 4 or more. SHB is not users' only financial tool.

User Interviews

Conducting interviews with 5 participants from different demographics, representing different perspectives on finance:

Determining features to prioritize

Throughout the initial survey as well as follow up interviews and in-person activities, relevance and social context drive engagement decisions more than convenience or logistics.

Personas

The financial management feature is very much reliant on the type of people who are using it, so we decided that building out potential personas would be essential. The 5 Personas here, made by the senior UX researcher, is focused on including both a diversity in life stage as well as mindset when it comes to financial management.

Moving forward, in order to focus on building out a detailed roadmaps, we decided to focus more on one key persona based on 2 criterias: SHB's existing customer base as well as SHB's current positioning as a bank.

User Journey

INSIGHTS

Money is personal

1.

Low financial literacy + low motivation means education must come to users.

Vietnamese users often lack both the knowledge and the drive to manage their finances proactively. Financial education can't be delivered as a course or a wall of information

-> Education needs to be woven into the process, surfacing when real needs arise.

2

The less they have to think about money, the better: automation is essential.

Users don't want to engage with finances — they want finances handled. Manual tracking feels tedious and it is easy for people to lose motivation midway.

-> The feature should support automation and offering insights when needed with minimal friction.

3

Money is scattered across many places , which means no single app sees the full picture.

Money decisions are deeply embedded in multigenerational family structures such as: sending money to parents or family in the countryside, managing shared household costs, inheriting savings attitudes from parents…

-> Integrate understanding of a familial approach to other features, such as automating certain work flows.

4

Financial management is, in many cases a family matter, not a solo act.

Users routinely hold accounts across 3–5 banking apps, and older generations keep wealth in real estate, land, and gold that never appears in any app.

-> Language used when offering suggestions and insights should reflect the fact that the bank may not see the whole picture + Allow users to log non-digital assets

LOW-FI

Translating research insights into prototypes

Determining features to prioritize

Using the Kano Model, I mapped out features across different pages like cash flow management and planning to prioritize based on the insights.

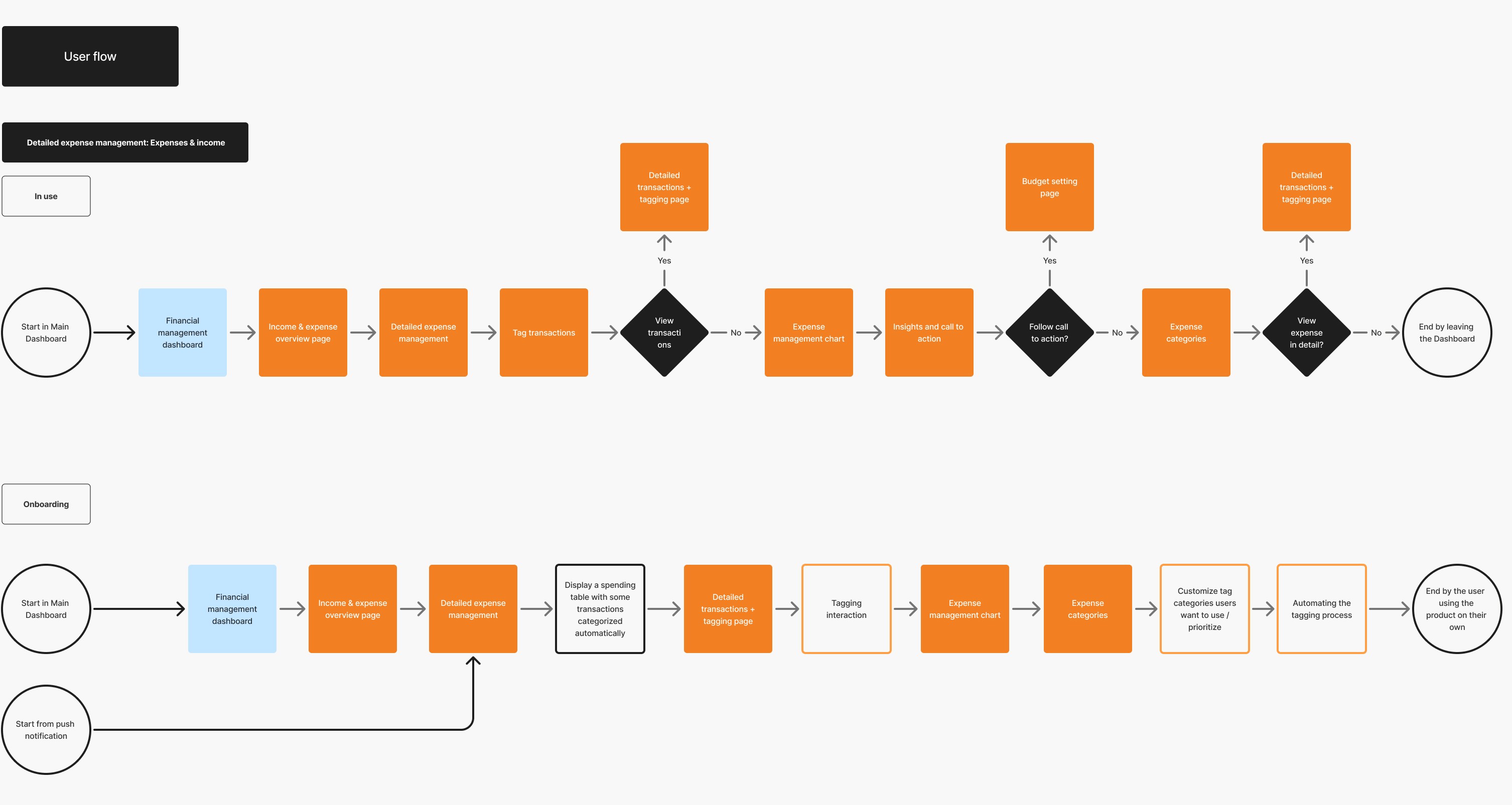

Information Architechture

User Flow

TESTING

A/B Testing: Visual solutions for micro-interactions

TEXT MENU

SHB's older, less tech-savvy clientele prefer more details for their actions

ICONS & NOTE MENU

Better feedback for visual appeal, however, lacked the context needed

MOVING BOX

Easier for users to track, immediate feedback helps with trust

STATIC BOX

Considered more stable but less visually intuitive because of distance

IMPACT

Designing solutions to bridge the old and the new across a product.

At SHB, I contributed to a shipped feature, owned the end-to-end design of a feature handed off, and presented user research to inform decisions on a core product initiative. My work was part of a broader shift toward more human-centered product development - helping one of Vietnam's leading commercial banks stay competitive in its digital transformation.

CONTRIBUTED TO A SHIPPED FEATURE RELEASED TO

200,000+ users

across Vietnam

PRESENTING RESEARCH & FINDINGS TO

12 domain experts across departments

LEARNING

Navigating complex problems to deliver simple solutions.

Cultural context plays a huge role in user behavior

Working on a financial management tool means features must be informed by cultural norms, which can only be uncovered by talking to real people.

Understanding diverse perspectives and habits

While people carry different expectations, experiences and needs, finding the common thread while honoring those differences matters.

Technical problems have a human core

Topics that seem dry and technical can carry real human weight: anxiety, confusion, and hope — sometimes the goal goes beyond completing a task.

Knowing when to push and challenge conventions.

It's important to advocate for your ideas and what you believe is valuable to the user, even in a room full of different perspectives and expertise.

MY TAKEAWAYS

This summer had been a meaningful experience for me. I learnt to:

Navigate agile workflows inside a large corporation mid-transformation

Get comfortable with the technical vocabulary of credit, loans, and banking products

Reconnect with why product design exists at all: not to ship features, but to understand people